Shareholders of Hudson Technologies would probably like to forget the past six months even happened. The stock dropped 30.5% and now trades at $5.49. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is now the time to buy Hudson Technologies, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Even though the stock has become cheaper, we're swiping left on Hudson Technologies for now. Here are three reasons why you should be careful with HDSN and a stock we'd rather own.

Why Is Hudson Technologies Not Exciting?

Founded in 1991, Hudson Technologies (NASDAQ:HDSN) specializes in refrigerant services and solutions, providing refrigerant sales, reclamation, and recycling.

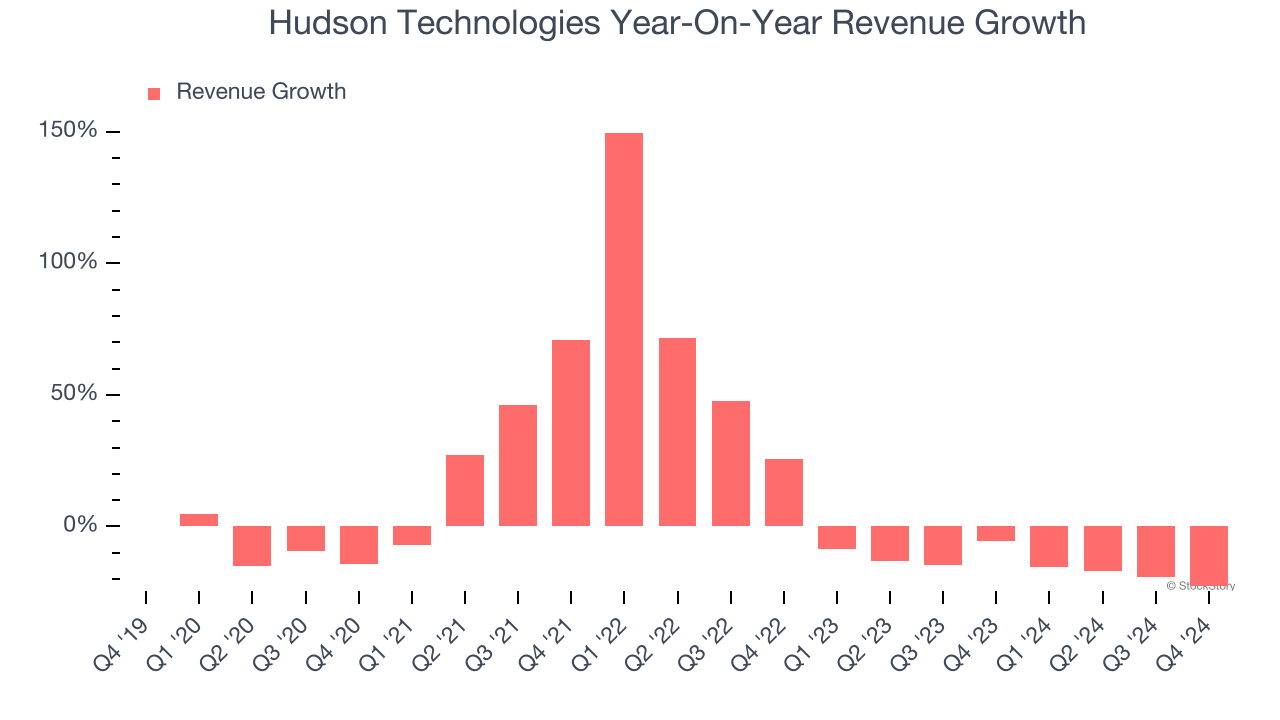

1. Revenue Tumbling Downwards

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. Hudson Technologies’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 14.6% over the last two years.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Hudson Technologies’s revenue to drop by 4.1%. While this projection is better than its two-year trend, it's hard to get excited about a company that is struggling with demand.

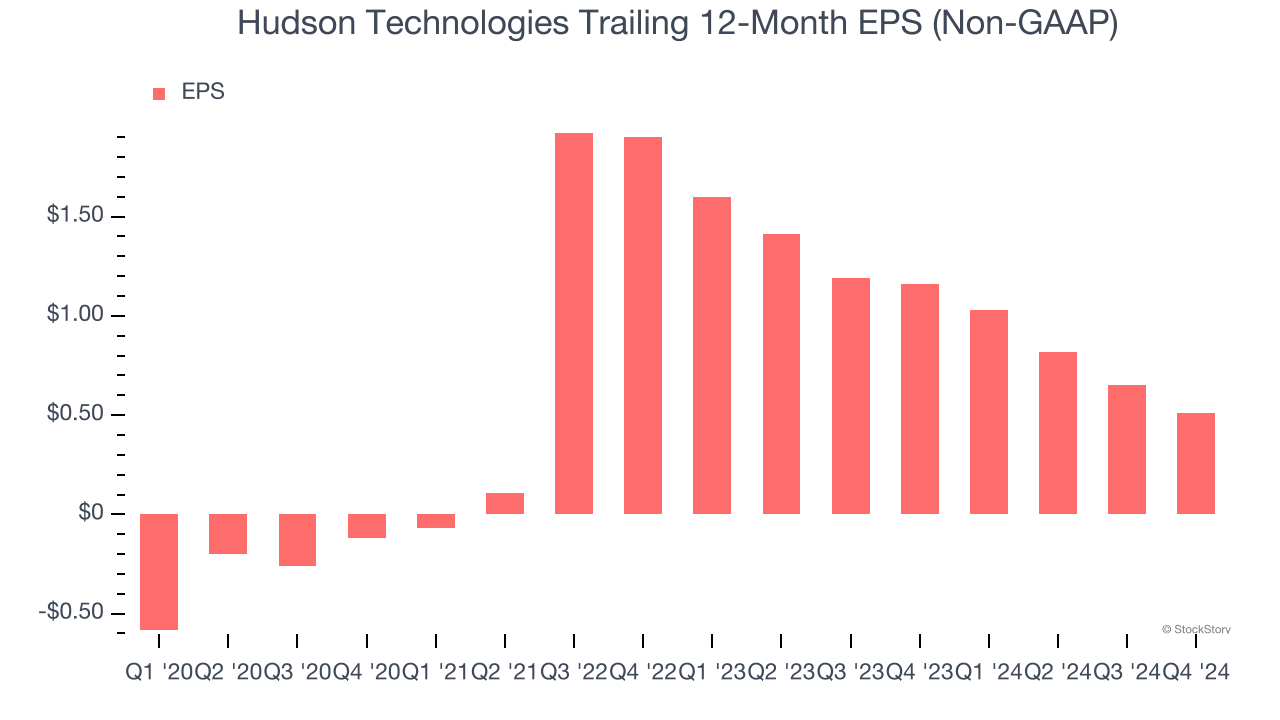

3. EPS Took a Dip Over the Last Two Years

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Sadly for Hudson Technologies, its EPS declined by more than its revenue over the last two years, dropping 48.2%. This tells us the company struggled to adjust to shrinking demand.

Final Judgment

Hudson Technologies’s business quality ultimately falls short of our standards. Following the recent decline, the stock trades at 14.2× forward price-to-earnings (or $5.49 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are more exciting stocks to buy at the moment. Let us point you toward a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Like More Than Hudson Technologies

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.