Earnings results often indicate what direction a company will take in the months ahead. With Q3 behind us, let’s have a look at Etsy (NASDAQ:ETSY) and its peers.

Marketplaces have existed for centuries. Where once it was a main street in a small town or a mall in the suburbs, sellers benefitted from proximity to one another because they could draw customers by offering convenience and selection. Today, a myriad of online marketplaces fulfill that same role, aggregating large customer bases, which attracts commission-paying sellers, generating flywheel scale effects that feed back into further customer acquisition.

The 13 online marketplace stocks we track reported a satisfactory Q3. As a group, revenues beat analysts’ consensus estimates by 2.8% while next quarter’s revenue guidance was in line.

Luckily, online marketplace stocks have performed well with share prices up 33.6% on average since the latest earnings results.

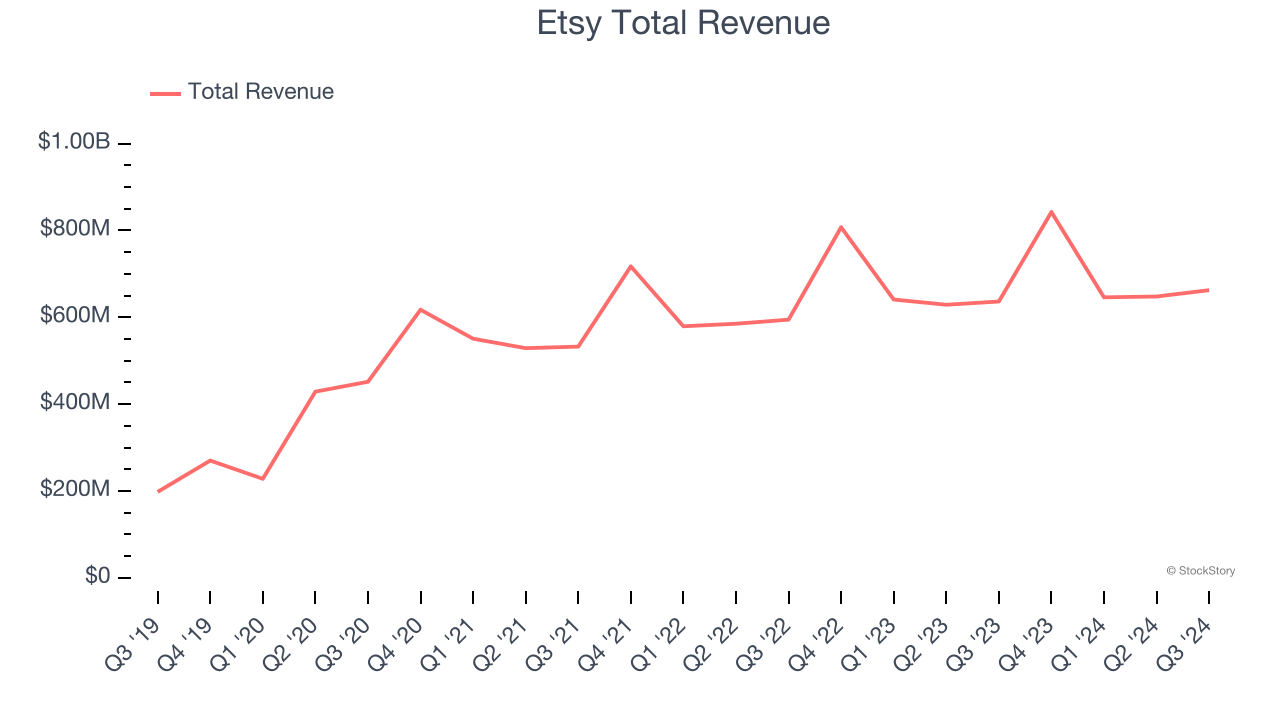

Etsy (NASDAQ:ETSY)

Founded by a struggling amateur furniture maker Robert Kalin and his two friends, Etsy (NASDAQ:ETSY) is one of the world’s largest online marketplaces, focusing on handmade or vintage items.

Etsy reported revenues of $662.4 million, up 4.1% year on year. This print exceeded analysts’ expectations by 1.5%. Despite the top-line beat, it was still a mixed quarter for the company with a solid beat of analysts’ EBITDA estimates but number of active buyers in line with analysts’ estimates.

"Our third quarter consolidated results came in roughly as anticipated, with some incremental pressure on Etsy marketplace year-over-year GMS, healthy growth in revenue, and continued strength in our adjusted EBITDA profitability," said Josh Silverman,

The stock is up 13.1% since reporting and currently trades at $54.26.

Is now the time to buy Etsy? Access our full analysis of the earnings results here, it’s free.

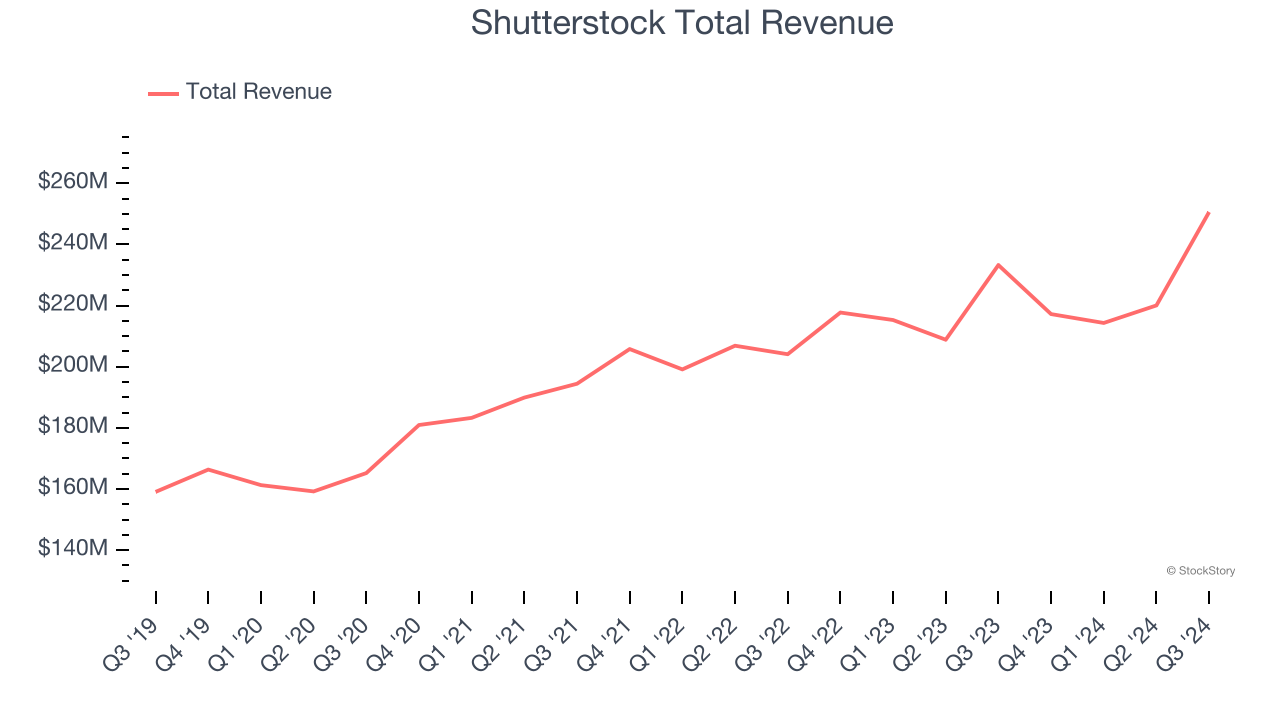

Best Q3: Shutterstock (NYSE:SSTK)

Originally featuring a library that included many of founder Jon Oringer’s photos, Shutterstock (NYSE:SSTK) is now a digital platform where customers can license and use hundreds of millions of pieces of content.

Shutterstock reported revenues of $250.6 million, up 7.4% year on year, outperforming analysts’ expectations by 5.1%. The business had a very strong quarter with an impressive beat of analysts’ EBITDA estimates and a solid beat of analysts’ number of paid downloads estimates.

The market seems happy with the results as the stock is up 8.9% since reporting. It currently trades at $32.14.

Is now the time to buy Shutterstock? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: MercadoLibre (NASDAQ:MELI)

Originally started as an online auction platform, MercadoLibre (NASDAQ:MELI) is a one-stop e-commerce marketplace and fintech platform in Latin America.

MercadoLibre reported revenues of $5.31 billion, up 35.3% year on year, exceeding analysts’ expectations by 2.5%. Still, it was a slower quarter as it posted a significant miss of analysts’ EBITDA estimates.

As expected, the stock is down 6% since the results and currently trades at $1,993.

Read our full analysis of MercadoLibre’s results here.

CarGurus (NASDAQ:CARG)

Bringing transparency to a sometimes opaque process, CarGurus (NASDAQ:CARG) is a digital marketplace where auto dealers can connect with potential customers and where car buyers can browse, purchase, and obtain financing.

CarGurus reported revenues of $231.4 million, up 5.4% year on year. This result topped analysts’ expectations by 3.2%. Taking a step back, it was a mixed quarter as it also recorded a solid beat of analysts’ EBITDA estimates but revenue guidance for next quarter missing analysts’ expectations.

The company reported 31,684 users, up 1.6% year on year. The stock is up 19.5% since reporting and currently trades at $39.89.

Read our full, actionable report on CarGurus here, it’s free.

EverQuote (NASDAQ:EVER)

Aiming to simplify a once complicated process, EverQuote (NASDAQ:EVER) is an online insurance marketplace where consumers can compare and purchase various types of insurance from different providers

EverQuote reported revenues of $144.5 million, up 163% year on year. This number surpassed analysts’ expectations by 2.9%. Overall, it was a very strong quarter as it also put up EBITDA guidance for next quarter exceeding analysts’ expectations.

EverQuote delivered the fastest revenue growth among its peers. The stock is up 21.5% since reporting and currently trades at $21.05.

Read our full, actionable report on EverQuote here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.