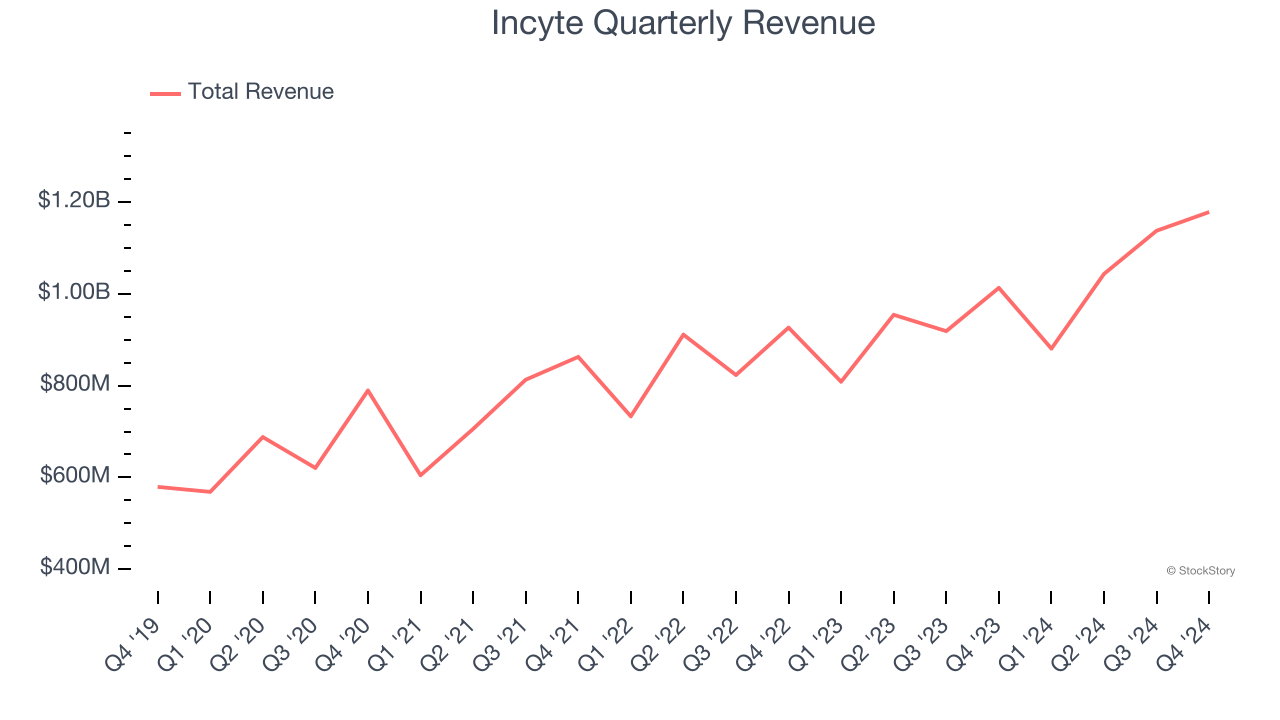

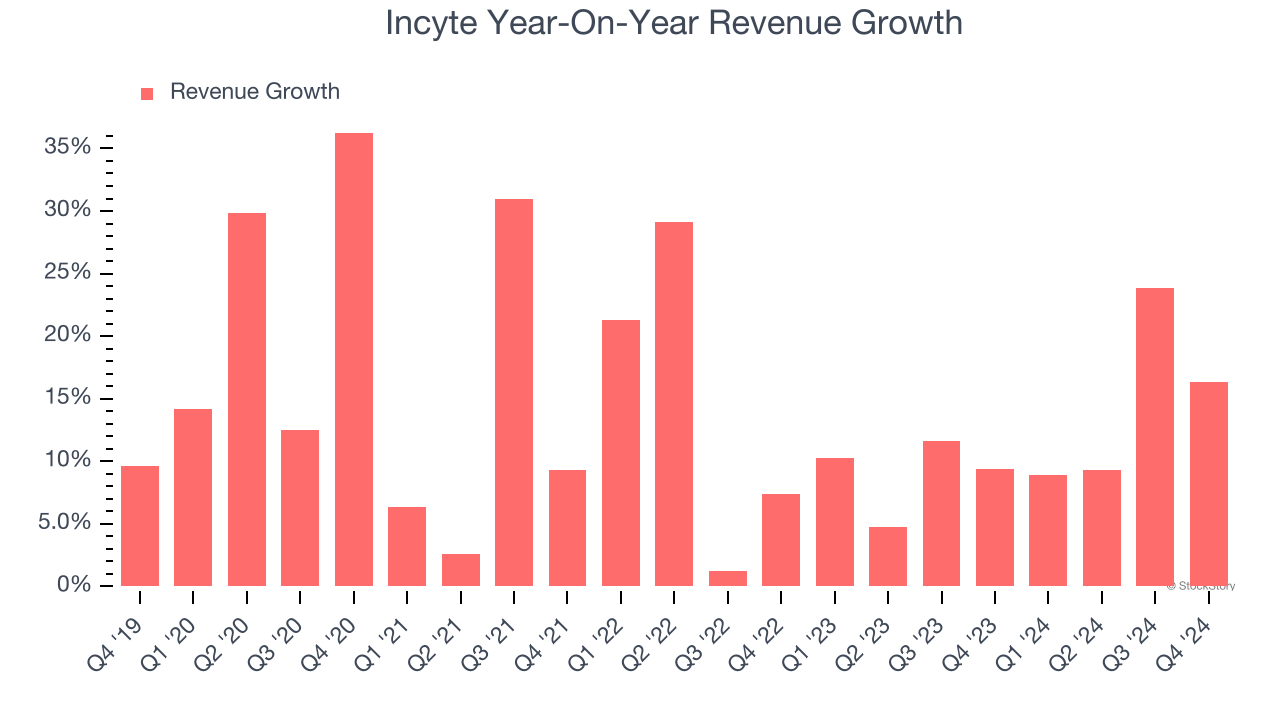

Biopharmaceutical company Incyte Corporation (NASDAQ:INCY) announced better-than-expected revenue in Q4 CY2024, with sales up 16.3% year on year to $1.18 billion. Its non-GAAP profit of $1.43 per share was 8% below analysts’ consensus estimates.

Is now the time to buy Incyte? Find out by accessing our full research report, it’s free.

Incyte (INCY) Q4 CY2024 Highlights:

- Revenue: $1.18 billion vs analyst estimates of $1.14 billion (16.3% year-on-year growth, 3% beat)

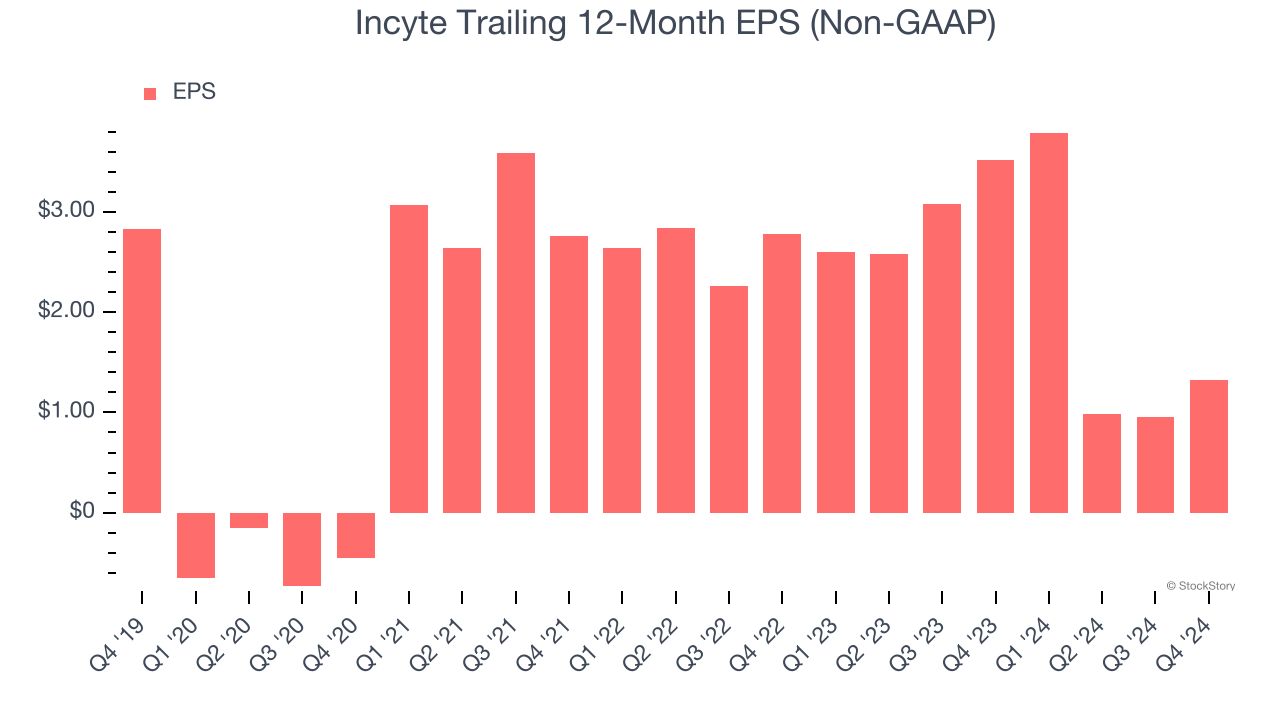

- Adjusted EPS: $1.43 vs analyst expectations of $1.55 (8% miss)

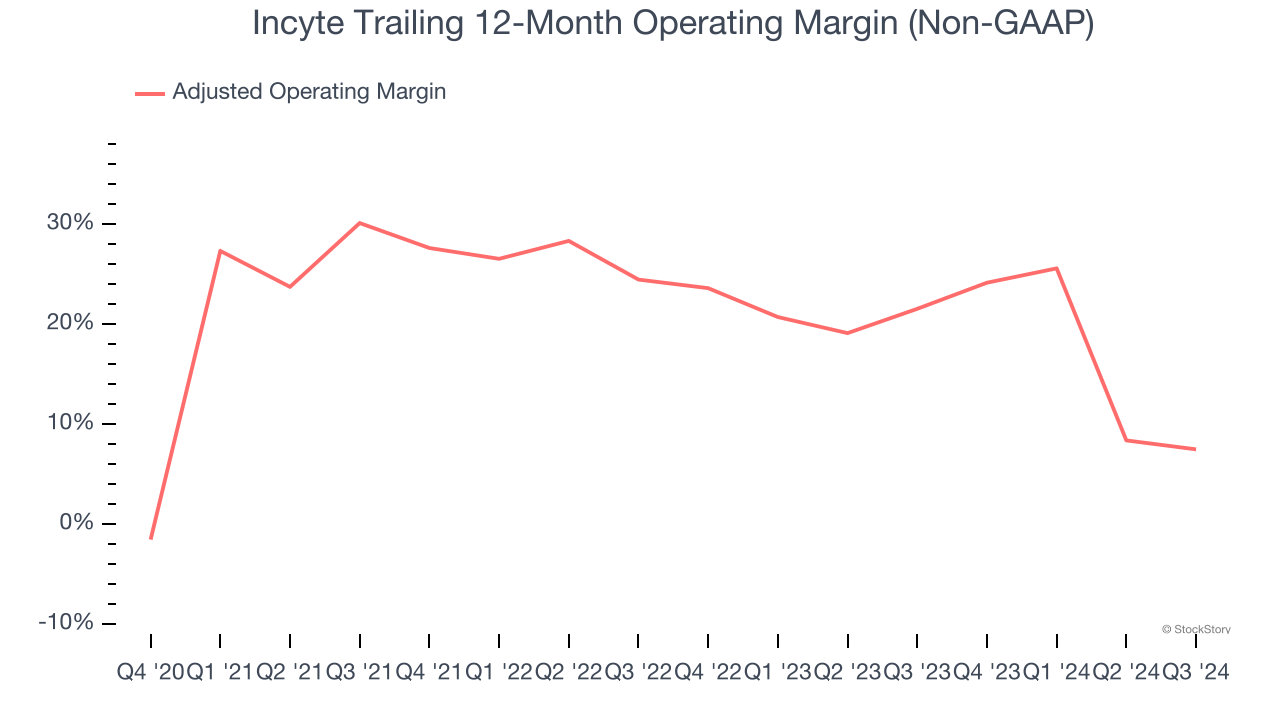

- Operating Margin: 25.6%, up from 18.5% in the same quarter last year

- Market Capitalization: $14.28 billion

"2024 was an important year for Incyte, with a 15% increase in total revenues, driven by strong growth from both Jakafi and Opzelura, as well as significant progress across our R&D pipeline," said Hervé Hoppenot, Chief Executive Officer, Incyte.

Company Overview

Founded in 1991, Incyte Corporation (NASDAQ:INCY) is a biopharmaceutical company that focuses on developing innovative therapies for oncology (cancer) and inflammation, with key products treating blood cancers and disorders, eczema, and other autoimmune skin disorders.

Immuno-Oncology

Over the next few years, immuno-oncology companies, which harness the immune system to fight illnesses such as cancer, faces strong tailwinds from advancements in precision medicine (including the use of AI to improve hit rates) and growing demand for treatments targeting rare diseases. However, headwinds such as rising scrutiny over drug pricing, regulatory unknowns, and competition from larger, more resourced pharmaceutical companies could weigh on growth.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Incyte’s 14.5% annualized revenue growth over the last five years was solid. Its growth beat the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Incyte’s annualized revenue growth of 11.8% over the last two years is below its five-year trend, but we still think the results were respectable.

This quarter, Incyte reported year-on-year revenue growth of 16.3%, and its $1.18 billion of revenue exceeded Wall Street’s estimates by 3%.

Looking ahead, sell-side analysts expect revenue to grow 9% over the next 12 months, a slight deceleration versus the last two years. Despite the slowdown, this projection is healthy and suggests the market is factoring in success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Adjusted Operating Margin

Incyte has managed its cost base well over the last five years. It demonstrated solid profitability for a healthcare business, producing an average adjusted operating margin of 15.9%.

Looking at the trend in its profitability, Incyte’s adjusted operating margin rose by 15 percentage points over the last five years, as its sales growth gave it immense operating leverage. Zooming into its more recent performance, however, we can see the company’s margin has decreased by 25.1 percentage points on a two-year basis. If Incyte wants to pass our bar, it must prove it can expand its profitability consistently.

in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Incyte, its EPS declined by 14.1% annually over the last five years while its revenue grew by 14.5%. However, its adjusted operating margin actually expanded during this time and it repurchased its shares, telling us the delta came from reduced interest expenses or taxes.

In Q4, Incyte reported EPS at $1.43, up from $1.06 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Incyte’s full-year EPS of $1.32 to grow 343%.

Key Takeaways from Incyte’s Q4 Results

We enjoyed seeing Incyte exceed analysts’ revenue expectations this quarter. On the other hand, its EPS missed significantly. Overall, this quarter could have been better, but the stock traded up 1.7% to $75.40 immediately after reporting.

Should you buy the stock or not? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.