What a brutal six months it’s been for Kimberly-Clark. The stock has dropped 23.2% and now trades at $107.08, rattling many shareholders. This might have investors contemplating their next move.

Is there a buying opportunity in Kimberly-Clark, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free for active Edge members.

Why Is Kimberly-Clark Not Exciting?

Despite the more favorable entry price, we're sitting this one out for now. Here are three reasons why KMB doesn't excite us and a stock we'd rather own.

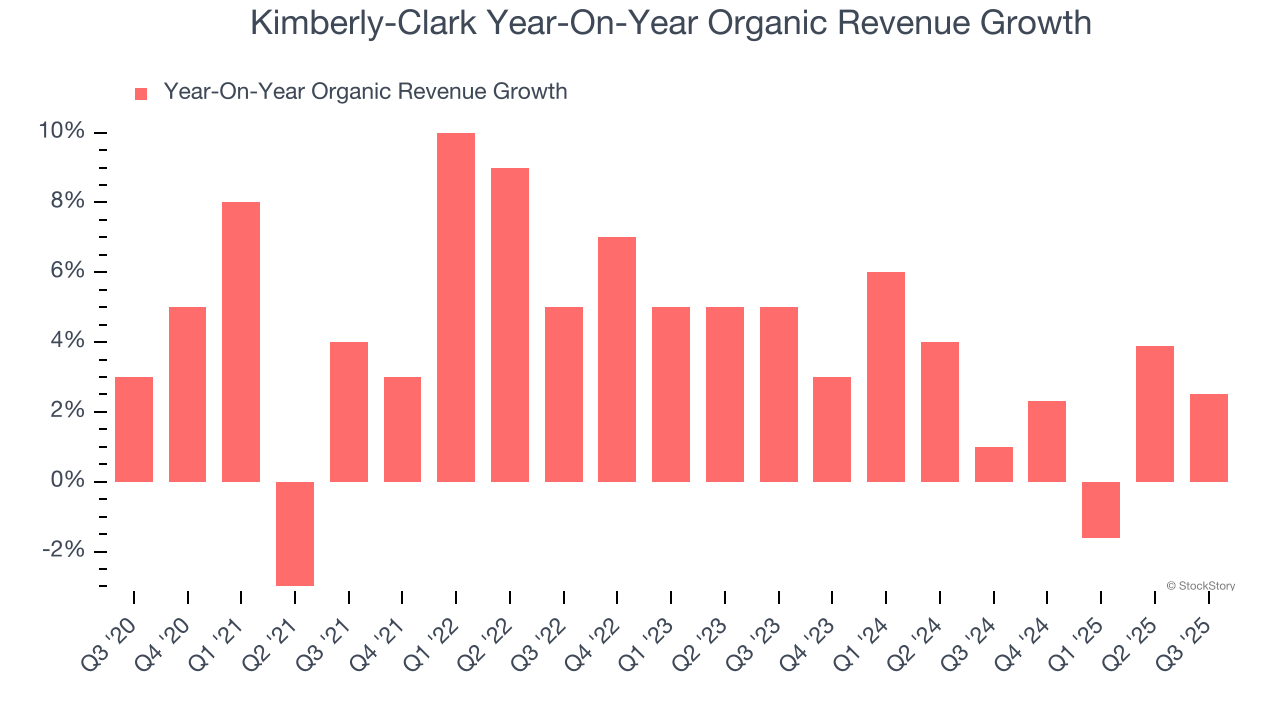

1. Slow Organic Growth Suggests Waning Demand In Core Business

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

The demand for Kimberly-Clark’s products has generally risen over the last two years but lagged behind the broader sector. On average, the company’s organic sales have grown by 2.6% year on year.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Kimberly-Clark’s revenue to rise by 2.1%. While this projection indicates its newer products will catalyze better top-line performance, it is still below the sector average.

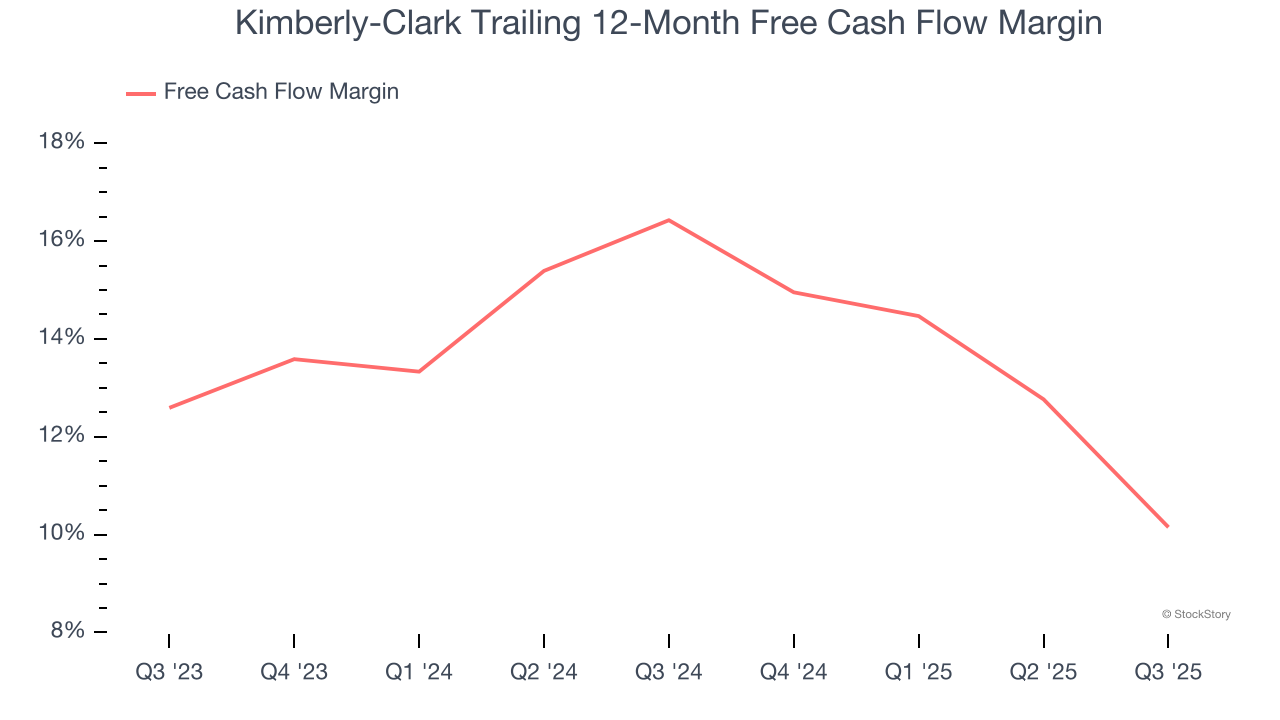

3. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Kimberly-Clark’s margin dropped by 6.3 percentage points over the last year. If its declines continue, it could signal increasing investment needs and capital intensity. Kimberly-Clark’s free cash flow margin for the trailing 12 months was 10.2%.

Final Judgment

Kimberly-Clark isn’t a terrible business, but it doesn’t pass our bar. Following the recent decline, the stock trades at 14× forward P/E (or $107.08 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're pretty confident there are superior stocks to buy right now. Let us point you toward one of Charlie Munger’s all-time favorite businesses.

High-Quality Stocks for All Market Conditions

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.