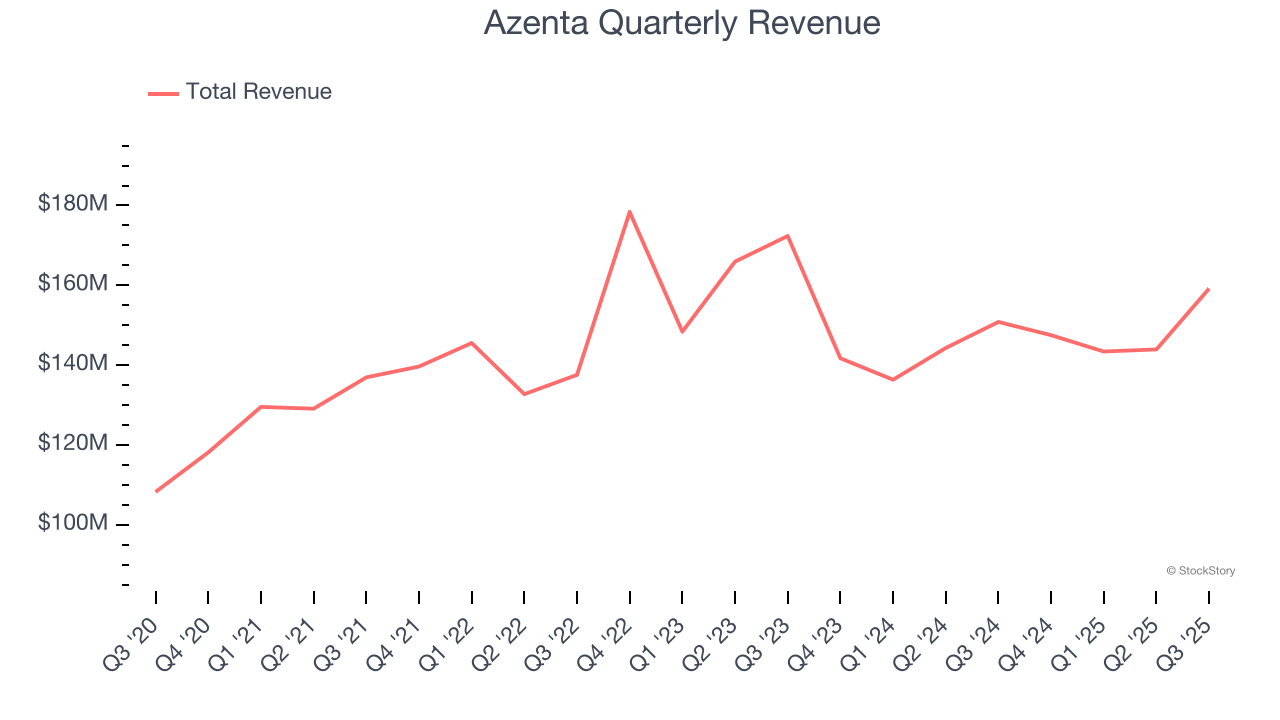

Life sciences company Azenta (NASDAQ:AZTA) reported Q3 CY2025 results topping the market’s revenue expectations, with sales up 5.5% year on year to $159.2 million. Its non-GAAP profit of $0.19 per share was in line with analysts’ consensus estimates.

Is now the time to buy Azenta? Find out by accessing our full research report, it’s free for active Edge members.

Azenta (AZTA) Q3 CY2025 Highlights:

- Revenue: $159.2 million vs analyst estimates of $156.7 million (5.5% year-on-year growth, 1.6% beat)

- Adjusted EPS: $0.19 vs analyst estimates of $0.20 (in line)

- Adjusted EBITDA: $20.71 million vs analyst estimates of $19.07 million (13% margin, 8.6% beat)

- Operating Margin: 1.2%, up from -2% in the same quarter last year

- Free Cash Flow was -$5.69 million, down from $1.66 million in the same quarter last year

- Market Capitalization: $1.38 billion

Company Overview

Serving as the guardian of some of medicine's most valuable materials, Azenta (NASDAQ:AZTA) provides biological sample management, storage, and genomic services that help pharmaceutical and biotechnology companies preserve and analyze critical research materials.

Revenue Growth

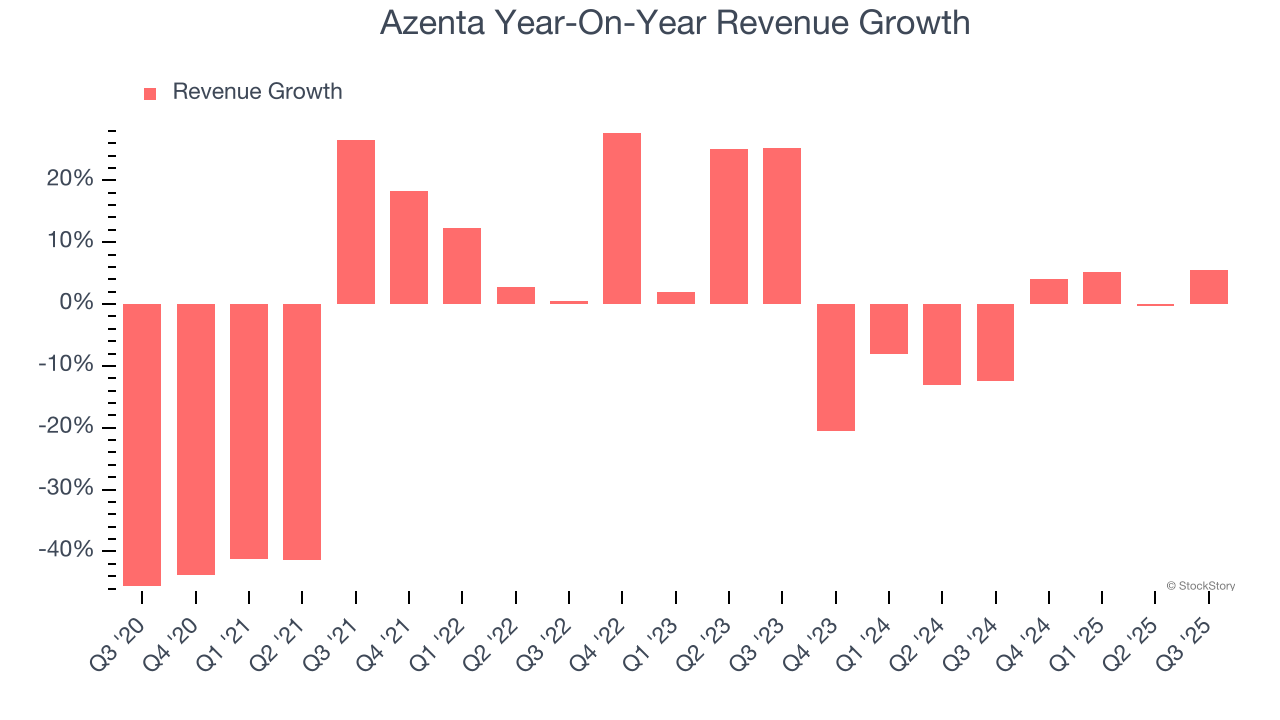

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Azenta’s demand was weak and its revenue declined by 4.8% per year. This wasn’t a great result and is a sign of poor business quality.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Azenta’s annualized revenue declines of 5.5% over the last two years align with its five-year trend, suggesting its demand has consistently shrunk.

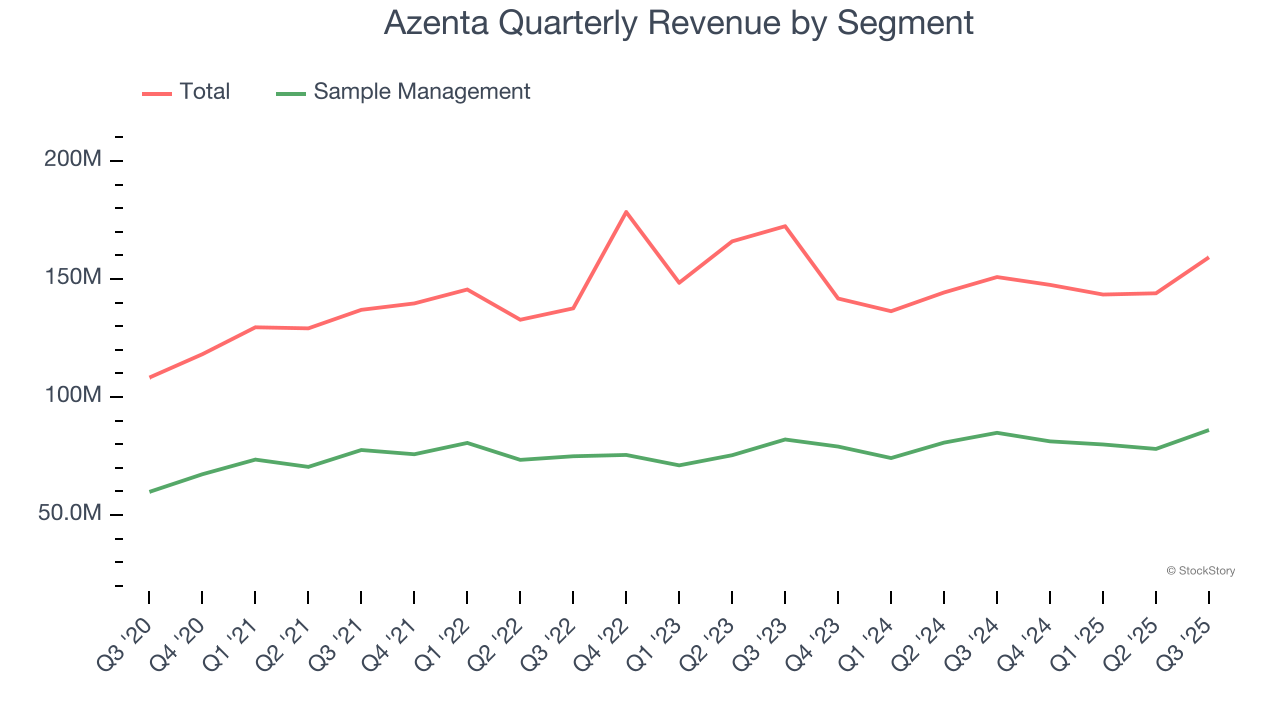

Azenta also breaks out the revenue for its most important segment, Sample Management. Over the last two years, Azenta’s Sample Management revenue averaged 3.5% year-on-year growth. This segment has outperformed its total sales during the same period, lifting the company’s performance.

This quarter, Azenta reported year-on-year revenue growth of 5.5%, and its $159.2 million of revenue exceeded Wall Street’s estimates by 1.6%.

Looking ahead, sell-side analysts expect revenue to grow 4.1% over the next 12 months. Although this projection suggests its newer products and services will catalyze better top-line performance, it is still below the sector average.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

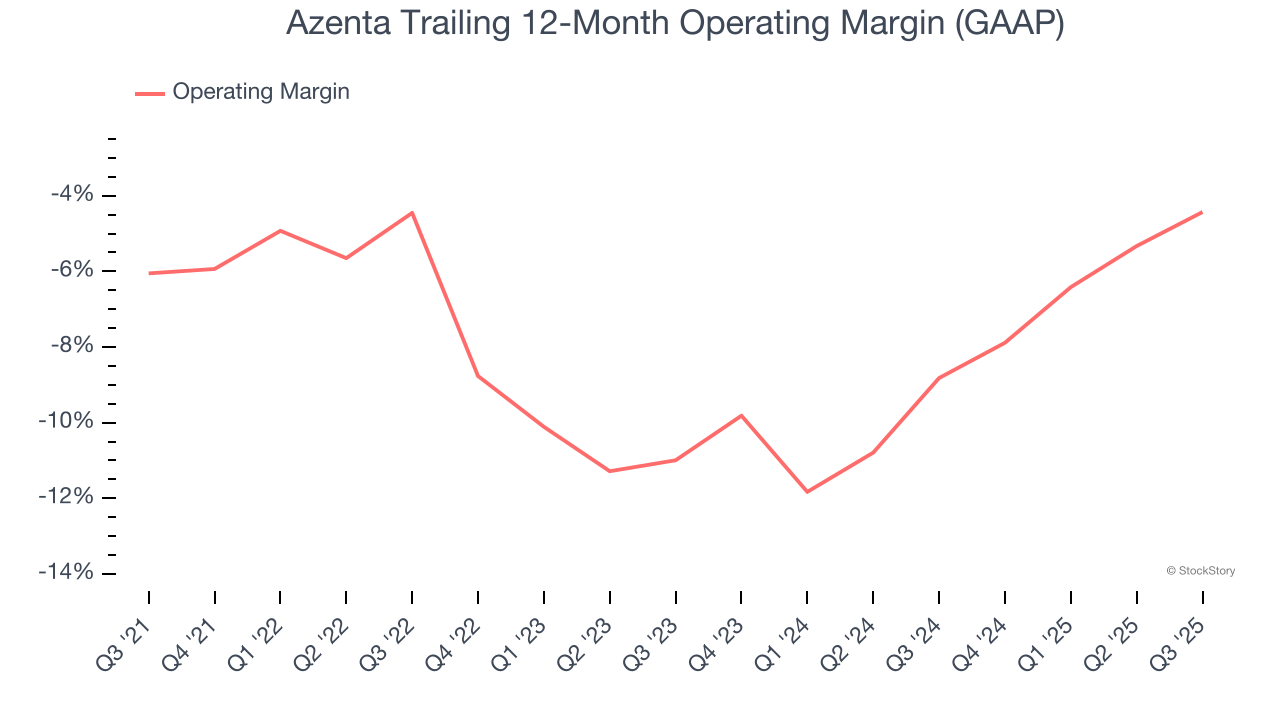

Although Azenta was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 7.1% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, Azenta’s operating margin rose by 1.6 percentage points over the last five years. This performance was mostly driven by its recent improvements as the company’s margin has increased by 6.6 percentage points on a two-year basis.

This quarter, Azenta generated an operating margin profit margin of 1.2%, up 3.2 percentage points year on year. This increase was a welcome development and shows it was more efficient.

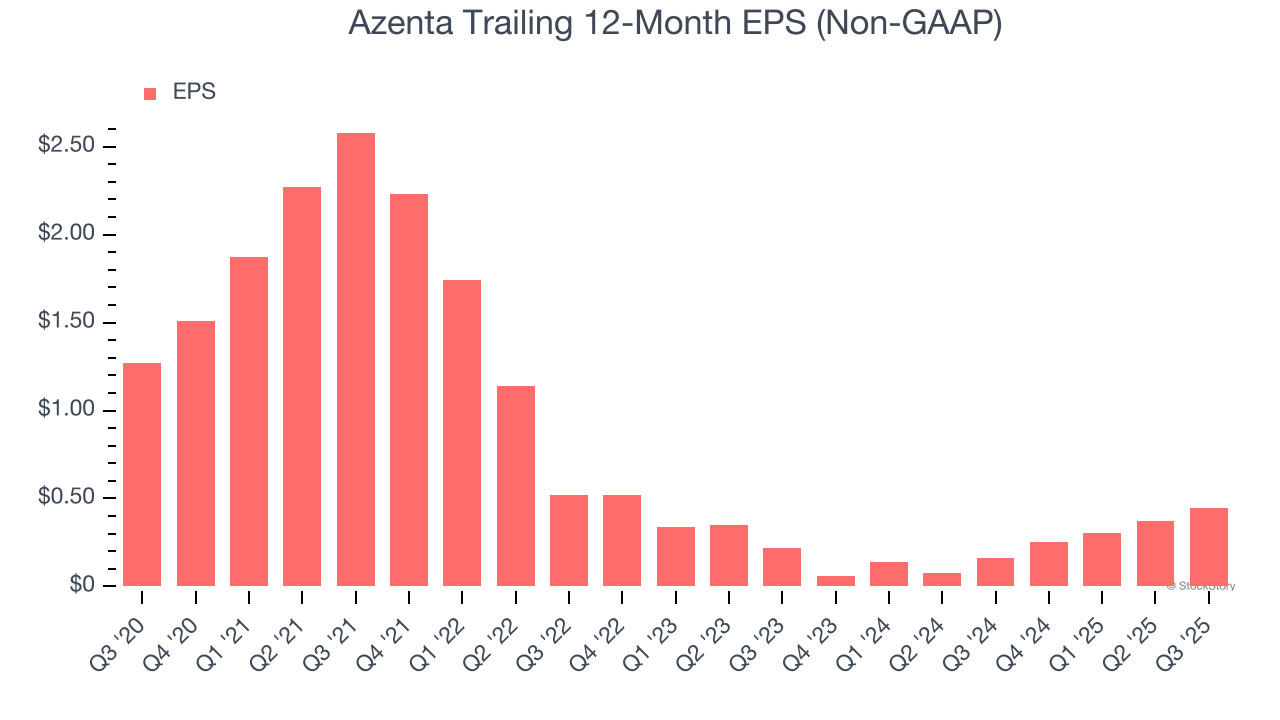

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Azenta, its EPS declined by 18.8% annually over the last five years, more than its revenue. We can see the difference stemmed from higher interest expenses or taxes as the company actually improved its operating margin and repurchased its shares during this time.

In Q3, Azenta reported adjusted EPS of $0.19, up from $0.11 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Azenta’s full-year EPS of $0.45 to grow 81.1%.

Key Takeaways from Azenta’s Q3 Results

It was encouraging to see Azenta beat analysts’ revenue expectations this quarter. EBITDA also exceeded expectations. On the other hand, its EPS was in line. Overall, this was a decent quarter. The stock remained flat at $30.04 immediately after reporting.

Should you buy the stock or not? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.