New York-based Apollo Global Management, Inc. (APO) is a private equity firm specializing in investments in credit, private equity, infrastructure, secondaries and real estate markets. Valued at $70.6 billion by market cap, the company focuses on investing in yield, hybrid, and equity markets to generate retirement and investment incomes.

Shares of this private equity giant have underperformed the broader market considerably over the past year. APO has declined 15.4% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 17.4%. In 2025, APO stock is down 25.3%, compared to the SPX’s 16% gains on a YTD basis.

Narrowing the focus, APO’s underperformance looks less pronounced compared to the Financial Select Sector SPDR Fund (XLF). The exchange-traded fund has gained about 10.8% over the past year. Moreover, the ETF’s 8.1% gains on a YTD basis outshine the stock’s double-digit dip over the same time frame.

APO’s weak performance is driven by rising expenses, acting as a headwind.

On Aug. 5, APO shares closed up by 2.5% after reporting its Q2 results. Its adjusted EPS of $1.92 surpassed the consensus estimate of $1.85. The total revenues stood at $6.8 billion, representing a 13.2% year-over-year increase.

For the current fiscal year, ending in December, analysts expect APO’s EPS to grow 9% to $7.18 on a diluted basis. The company’s earnings surprise history is mixed. It beat the consensus estimate in two of the last four quarters while missing the forecast on two other occasions.

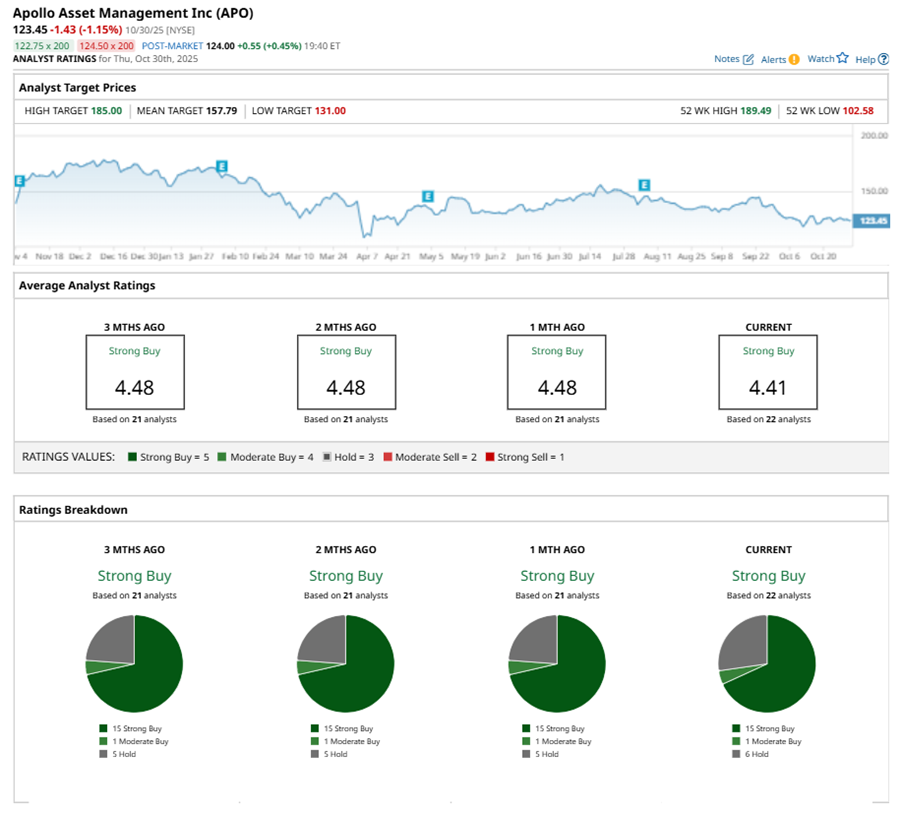

Among the 22 analysts covering APO stock, the consensus is a “Strong Buy.” That’s based on 15 “Strong Buy” ratings, one “Moderate Buy,” and six “Holds.”

The configuration has been reasonably stable over the past three months.

On Oct. 21, Morgan Stanley (MS) kept an “Equal Weight” rating on APO and lowered the price target to $151, implying a potential upside of 22.3% from current levels.

The mean price target of $157.79 represents a 27.8% premium to APO’s current price levels. The Street-high price target of $185 suggests an ambitious upside potential of 49.9%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart